Präsentation herunterladen

Die Präsentation wird geladen. Bitte warten

1

WS 2015-16 Kunibert Raffer Folien zur Vorlesung: Grundlagen der Entwicklungsökonomie Teil II © K. Raffer 2015

3

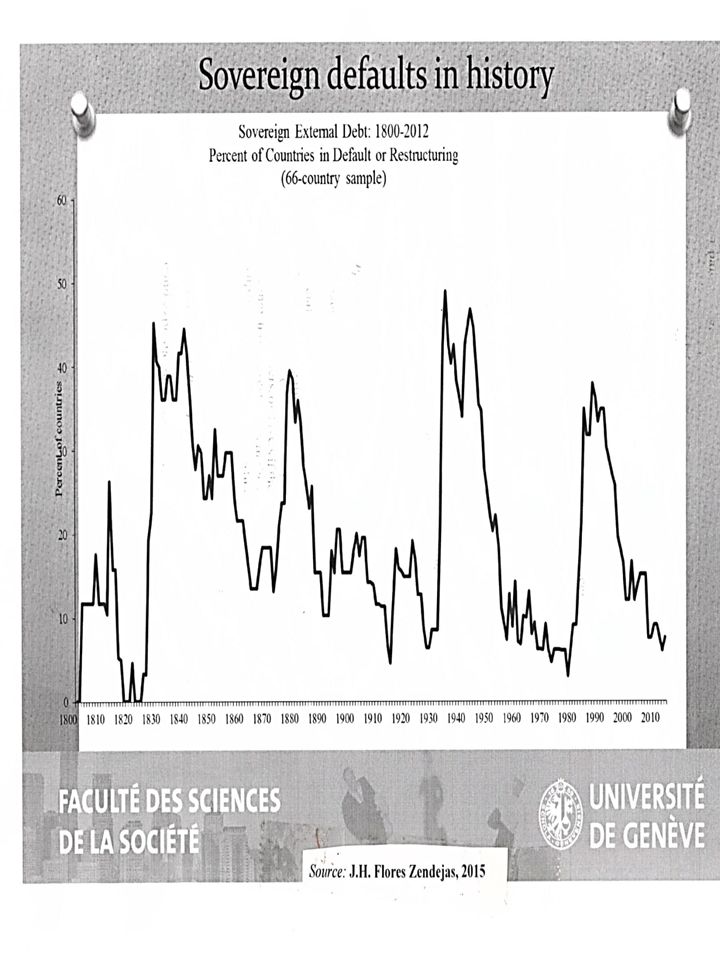

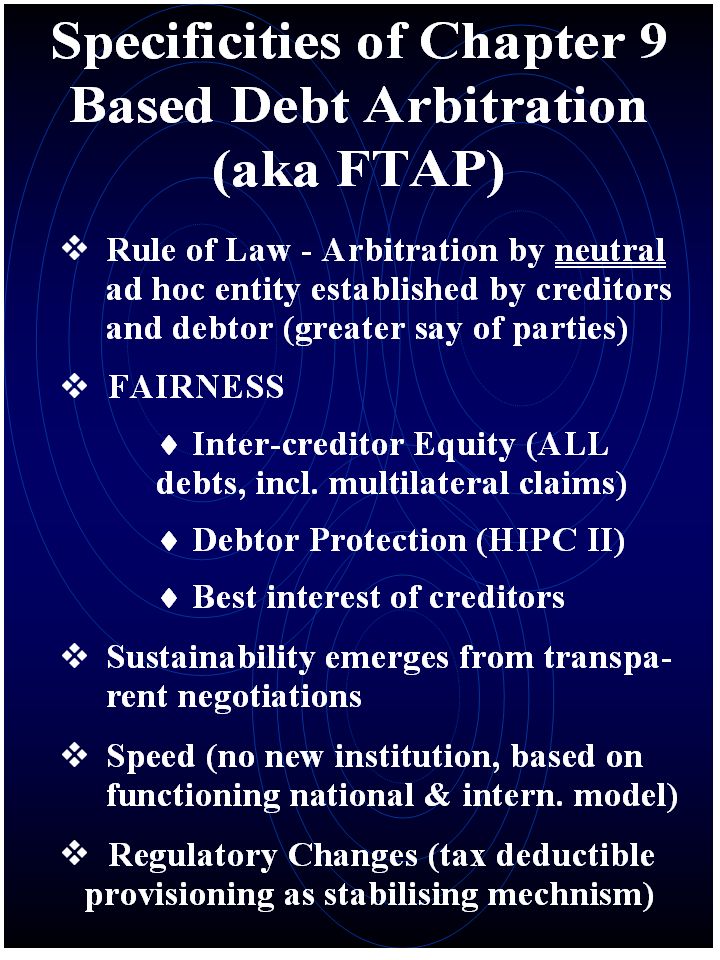

Waves of Resource Flows Pearson Report 1969 (official credits) Euromarket (private – syndicated – bank credits) IFIs after 1982 (public money) Bonds during the 1990s (private money, public at large) End of the line (need to find a way of assigning losses) Globalising insolvency procedures: Chapter 9 based debt arbitration SDRM Copyright: K. Raffer

7

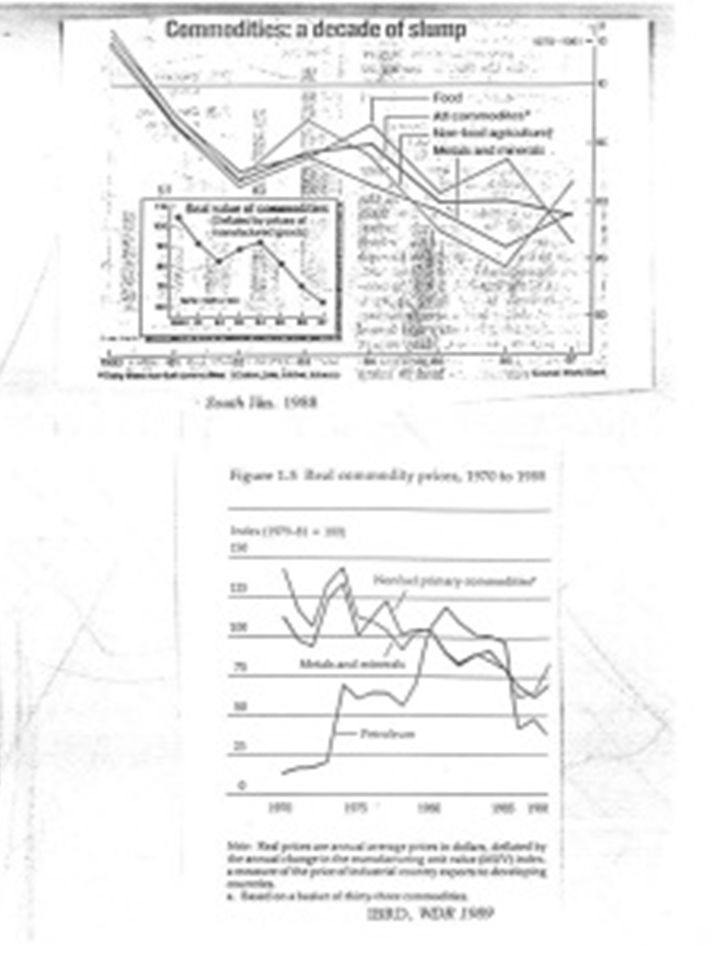

Kürzungen von Umweltausgaben wegen Schuldendrucks/ "Strukturanpassung„ Kürzung von Ausgaben für Umweltschutz z.B.: Brasilien kürzte Budget der Umweltagentur Waldbrand im Parque das Emas: erst nachdem über ein Drittel der 335.000 Morgen brannten rückte Feuerwehr mit 70 Mann und EINEM Feuerwehrauto aus, das Wassernachschub aus 25 Meilen Entfernung holen mußte Schuldendruck (Senator Bill Bradley: "desperation exports") führt zu Raubbau an Umwelt (allerdings gab es Umweltzer- störung schon vor Schuldenkrise!) und Exporten zu ungün- stigsten Bedingungen (v. Ungleicher Tausch) Westl. Hemisphäre: Auslandsverschuldung/Exporte 360% Schuldendienstquote: 198033,7 % 198251,3 % 1986> 51% „virtually the entire burden“ of adjustment on debtors; adjustment „involved mostly import contraction rather than export expansion“; this „will prolong rather than resolve the debt crisis“, „vicious circle of reduced imports and reduced export potential“ (GATT 1986, pp.25f) 1985: gross capital formation/GDP just over 2/3 of 1980 value IBRD (1988) „even minimal replacements may no longer occur in important sectors“; „severity of this prolonged economic slump already surpasses that of the Great Depression in industrial countries“; „already taken a heavy toll on growth … will continue to hold back future growth“

Westl. Hemisphäre: Auslandsverschuldung/Exporte 360% Schuldendienstquote: ,7 % ,3 % 1986> 51% „virtually the entire burden of adjustment on debtors; adjustment „involved mostly import contraction rather than export expansion ; this „will prolong rather than resolve the debt crisis , „vicious circle of reduced imports and reduced export potential (GATT 1986, pp.25f) 1985: gross capital formation/GDP just over 2/3 of 1980 value IBRD (1988) „even minimal replacements may no longer occur in important sectors ; „severity of this prolonged economic slump already surpasses that of the Great Depression in industrial countries ; „already taken a heavy toll on growth … will continue to hold back future growth .")

8

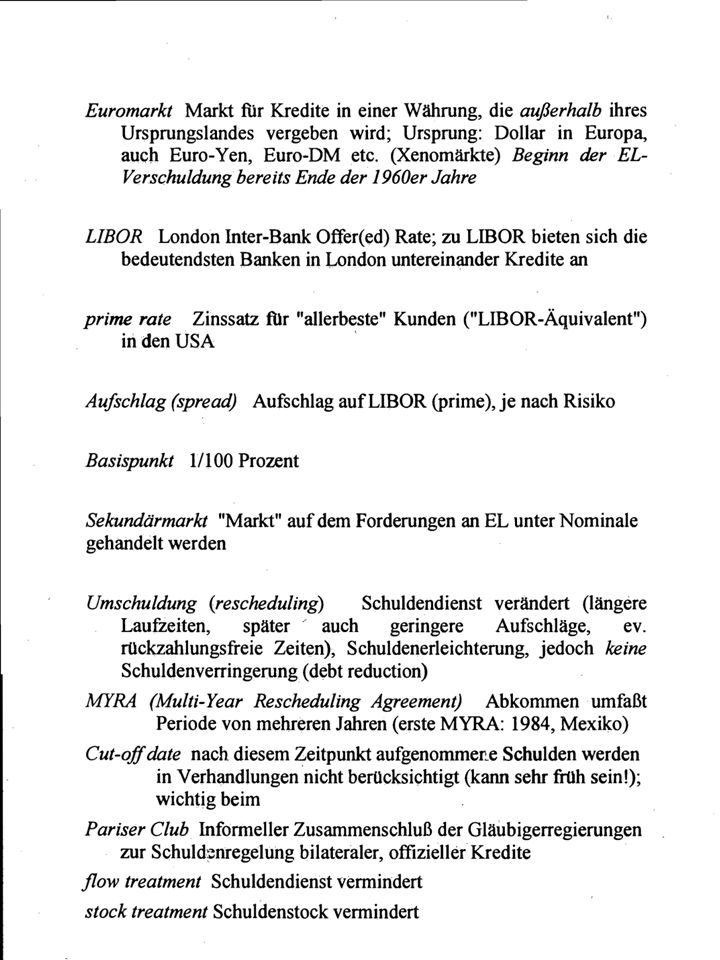

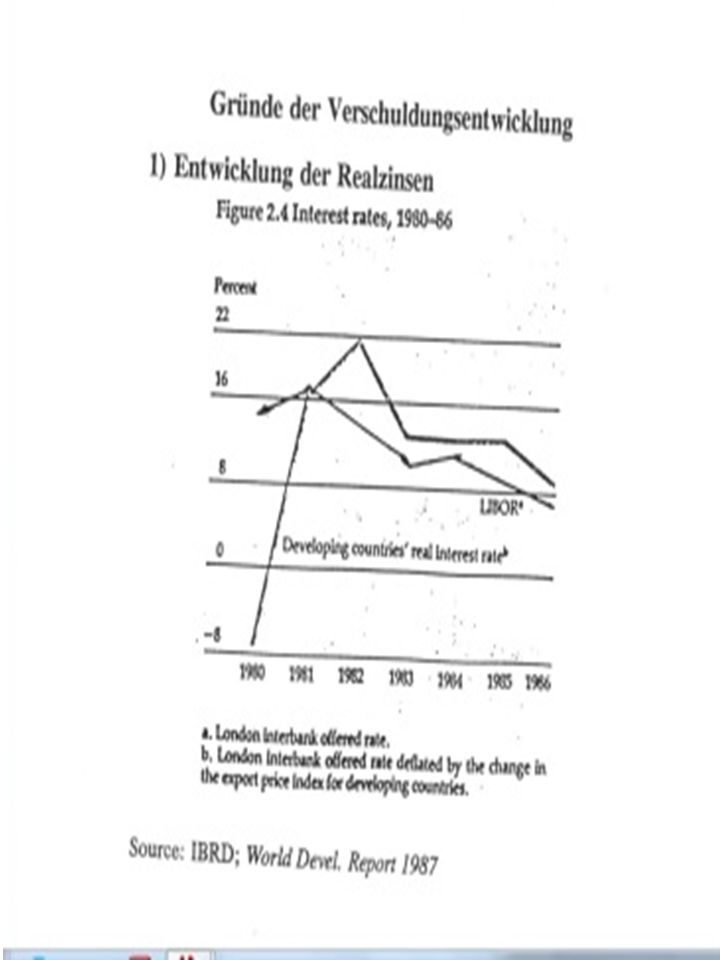

Illiquiditätstheorie William R. Cline (US Treasury Secretary James Baker, BWIs); optimistic assumptions regarding debtors' export volumes and prices, or relatively high growth in OECD countries, Cline (1985) claimed just before the 1985 IMF/IBRD meeting that by the late 1980s debt-export ratios would be back to levels previously associated with creditworthiness. Optimistically he concluded: ‘The emerging evidence in 1983-84 has tended to confirm the analysis that the debt problem is one of illiquidity and subject to improve-ment as international recovery takes place.’ (ibid., p.187) 1985: Baker „Plan“ -continued central role of the IMF together with multilateral development banks & more intensive IMF -IBRD collaboration -countries would “grow out of debts” -additional net lending of $29 billion over three years for some countries (unclear which) - Commercial banks: lend $20 billion, IFIs: $9 billion Put into perspective: Mexico alone paid $9.4 billion in interest (1985), her total debt service was $14.5 billion, Brazil's 10.3 billion Speisekartenansatz (menu approach)

; optimistic assumptions regarding debtors export volumes and prices, or relatively high growth in OECD countries, Cline (1985) claimed just before the 1985 IMF/IBRD meeting that by the late 1980s debt-export ratios would be back to levels previously associated with creditworthiness. Optimistically he concluded: ‘The emerging evidence in has tended to confirm the analysis that the debt problem is one of illiquidity and subject to improve-ment as international recovery takes place.’ (ibid., p.187) 1985: Baker „Plan -continued central role of the IMF together with multilateral development banks & more intensive IMF -IBRD collaboration -countries would grow out of debts -additional net lending of $29 billion over three years for some countries (unclear which) - Commercial banks: lend $20 billion, IFIs: $9 billion Put into perspective: Mexico alone paid $9.4 billion in interest (1985), her total debt service was $14.5 billion, Brazil s 10.3 billion Speisekartenansatz (menu approach).")

9

Schulden-Eigentum-Konversion (SEK) (Debt Equity Swap) Bank / \ U kauft von B Nominale Kreditschuld 100 Mio. $ 100 Mio $ zum Sekundärmarktkurs (50 Mio.) S -> B / \ Unternehmen - erhält für Nominale - Schuldnerland Inlandswährung (ev. Abzüge) Varianten: debt for nature debt for charity Venice Terms des Pariser Clubs (1987): volle Rückzahlung, aber verlängerte Fälligkeit für arme Staaten (cf “Baker Plan”) WENDE 1988 und 1989 1988 Toronto Bedingungen (und Mexiko, noch unter Baker) 1989 Bresser Perreira-Miyazawa-BRADY Plan SCHULDENERLASZ NOTWENDIG UND UNUMGÄNGLICH

S -> B / \ Unternehmen - erhält für Nominale - Schuldnerland Inlandswährung (ev. Abzüge) Varianten: debt for nature debt for charity Venice Terms des Pariser Clubs (1987): volle Rückzahlung, aber verlängerte Fälligkeit für arme Staaten (cf Baker Plan ) WENDE 1988 und Toronto Bedingungen (und Mexiko, noch unter Baker) 1989 Bresser Perreira-Miyazawa-BRADY Plan SCHULDENERLASZ NOTWENDIG UND UNUMGÄNGLICH.")

10

TORONTO BEDINGUNGEN reduction of official debts owed by poor (so-called ‘IDA-only’) countries to members of the Paris Club Options -1/3 of the stock of eligible debts -equivalent reduction of the rate of interest -On US insistence a third option was agreed on, which was considered equal: stretched maturities and grace periods of 14 years BRADY“ PLAN Schuldenreduktion & Verbriefung (Secutrisation) Erster "Brady-Plan" für Mexiko, Optionen: 1) Umtausch in Staatsobligationen mit 35% Abschlag vom Nominale (discount bond, 40%) 2) Zinsreduktion bei unverändertem Nominale (par bond, 6,25% fix, 47%) [beide Obligationen ohne jährliche Ammortisationszahlungen] 3) Neues Geld (13%)

![TORONTO BEDINGUNGEN reduction of official debts owed by poor (so-called ‘IDA-only’) countries to members of the Paris Club Options -1/3 of the stock of eligible debts -equivalent reduction of the rate of interest -On US insistence a third option was agreed on, which was considered equal: stretched maturities and grace periods of 14 years BRADY PLAN Schuldenreduktion & Verbriefung (Secutrisation) Erster Brady-Plan für Mexiko, Optionen: 1) Umtausch in Staatsobligationen mit 35% Abschlag vom Nominale (discount bond, 40%) 2) Zinsreduktion bei unverändertem Nominale (par bond, 6,25% fix, 47%) [beide Obligationen ohne jährliche Ammortisationszahlungen] 3) Neues Geld (13%)](http://images.slideplayer.org/27/9209307/slides/slide_10.jpg "TORONTO BEDINGUNGEN reduction of official debts owed by poor (so-called ‘IDA-only’) countries to members of the Paris Club Options -1/3 of the stock of eligible debts -equivalent reduction of the rate of interest -On US insistence a third option was agreed on, which was considered equal: stretched maturities and grace periods of 14 years BRADY PLAN Schuldenreduktion & Verbriefung (Secutrisation) Erster Brady-Plan für Mexiko, Optionen: 1) Umtausch in Staatsobligationen mit 35% Abschlag vom Nominale (discount bond, 40%) 2) Zinsreduktion bei unverändertem Nominale (par bond, 6,25% fix, 47%) [beide Obligationen ohne jährliche Ammortisationszahlungen] 3) Neues Geld (13%)")

11

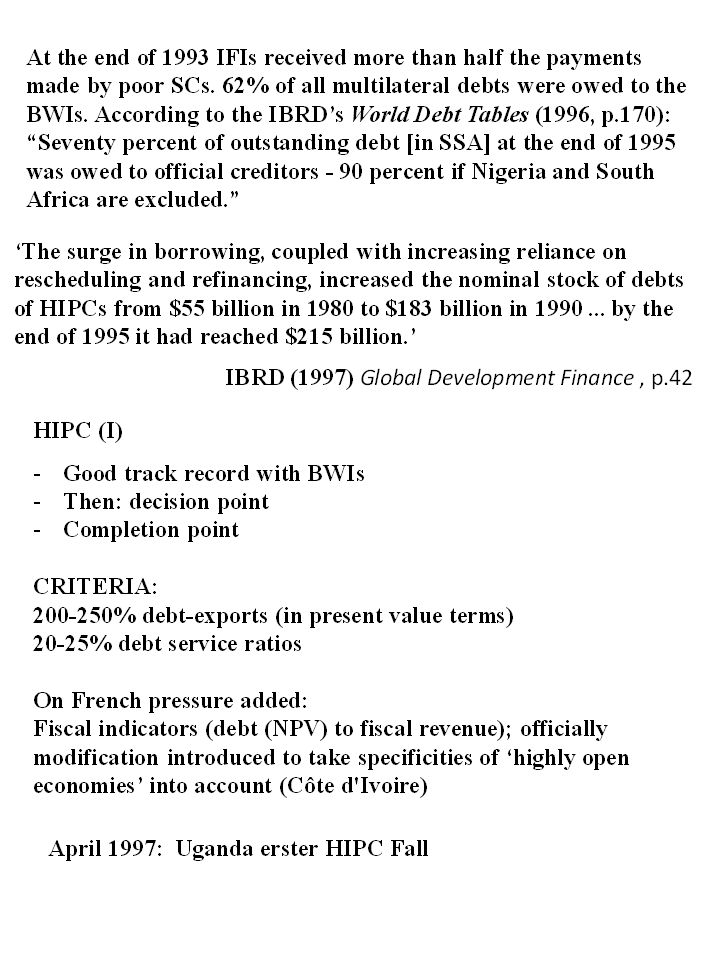

1991 Trinidad-Bedingungen: weitere Erleichterungen der Toronto- Bedingungen (2/3 Nachlaß), auch von G7-Ländern im Juli in London empfohlen; statt dessen: Einigung im Pariser Klub auf sog. Intermediären Trinidad-Bedingungen (auch London Bedingungen, Enhanced TT) 1994 Neapel-Bedingungen: 50 bis 67 Prozent Nachlaß (bis zu 80 % vorgeschlagen, vorerst nicht akzeptiert); Erhöhung im Rahmen der Debatte um mulitlaterale Schulden; Problem: cut-off date! 1996 Lyon Bedingungen (80%) nur für HIPCs 1990 Houston-Bedingungen: bereits für Länder mittleren Einkommens (Lower-Middle-Income Countries); Umschuldungen, bis zu 20 Jahre Rückzahlungszeitraum mit bis zu 10 Jahren Tilgungsfreiheit 2003 Evian Approach for non-HIPC countries; Paris Club eventually declared that the “adjustment of the ‘cut-off date’ will also be actively considered.” 1995-6 HIPC Multilaterale Schulden einbezogen!!!

1994 Neapel-Bedingungen: 50 bis 67 Prozent Nachlaß (bis zu 80 % vorgeschlagen, vorerst nicht akzeptiert); Erhöhung im Rahmen der Debatte um mulitlaterale Schulden; Problem: cut-off date Lyon Bedingungen (80%) nur für HIPCs 1990 Houston-Bedingungen: bereits für Länder mittleren Einkommens (Lower-Middle-Income Countries); Umschuldungen, bis zu 20 Jahre Rückzahlungszeitraum mit bis zu 10 Jahren Tilgungsfreiheit 2003 Evian Approach for non-HIPC countries; Paris Club eventually declared that the adjustment of the ‘cut-off date’ will also be actively considered HIPC Multilaterale Schulden einbezogen!!!.")

22

1) Misnomer: a) Euro NEVER in danger b) Not one but two (types of) crises ▬► austerity therefore NOT the one way out, two “recipes” needed Debunking Myths about “Eurocrisis” 2)Insolvency of euro-members can and must be averted as this would destroy the common currency - meanwhile: 2(!) PSIs in Greece!!! 3) Private Sector Involvement 4) Breaking the Law ( Art. 125 Lisbon Treaty) was allegedly “necessary” (other view: ECJ)

Private Sector Involvement 4) Breaking the Law ( Art. 125 Lisbon Treaty) was allegedly necessary (other view: ECJ).")

23

Currency NOT in Danger: NOT Crisis of Euro US: single currency era with several members more or less bankrupt, and on which untrue assertions abound The Union (Washington) DOES NOT bail out - 11 th Amendment NO “debt caused” TRANSFERS TO STATES!!! Union pays, of course, its OWN expenditures (federal agencies such as FBI, Coast Guard, CIA; individual entitlements such as Medicaid, unemployment benefits) in (NOT to) bankrupt States States DO NOT have to have a balanced budget - National Con-ference of State Legislatures: unclear which States have this re-striction on operating budgets – “Less attention (if any) is given to the question of whether a state’s entire budget is in balance.” “The common state practice is to consider that borrowing for capital expenditure does not violate the principle of maintaining a balanced budget… Borrowing for capital expenditure does not legally violate state balanced budget provisions.”

in (NOT to) bankrupt States States DO NOT have to have a balanced budget - National Con-ference of State Legislatures: unclear which States have this re-striction on operating budgets – Less attention (if any) is given to the question of whether a state’s entire budget is in balance. The common state practice is to consider that borrowing for capital expenditure does not violate the principle of maintaining a balanced budget… Borrowing for capital expenditure does not legally violate state balanced budget provisions. .")

24

1)Greece - “Latin American” crisis 2 ) Spain, Ireland (Iceland) – “Asian/Chilean” crisis Two Types of Crisis ==► two different sets of strategies Type 2 - Iceland’s case: “Private creditors ended up shouldering most of the losses relating to the failed banks, and today Iceland is experiencing a moderate recovery.” IMF Survey online, 3 November, 2011 Capital controls; referenda; fiscal policy NOT tightened during first year of the programme; - return to capital markets 2011 “Iceland set an example by managing to preserve, and even strengthen, its welfare state during the crisis.” ibid. Special prosecutor appointed “to seek out those who had broken the law and within a year that Office had become the largest judicial entity in Iceland” - Special commission, headed by a Supreme Court judge, established to examine conduct of everyone

25

The Case of Iceland General government expenditure on social protection, health and education (% of GDP) Source: Statistics Iceland, General Government Finances 2013, revision, 23 September 2014

Source: Statistics Iceland, General Government Finances 2013, revision, 23 September 2014")

26

Public health expenditures: 7.22% of GDP (2008) - 6.99% (2012) “As the economy contracted by about eight per cent between 2008 and 2010, it should be noted that in real terms painful cuts were made to public health services and education. Compared to 2007 expenditures, funds spend in 2013 on public health care and education were by 7.2 and 8.3 per cent lower” Bohoslavsky, Report, 2015, p.11 2007: central Government debt 43% of GDP – 109% in 2013 (33 % in foreign currency) 2010: Supreme Court - foreign currency indexed loans offered by Icelandic banks to many clients for buying vehicles and houses illegal Savings deposits of Icelandic customers secured; debt of many local businesses largely written off 2009: Welfare Watch - monitor social impact of crisis, advice State institutions, coordinate targeted interventions on the ground

2010: Supreme Court - foreign currency indexed loans offered by Icelandic banks to many clients for buying vehicles and houses illegal Savings deposits of Icelandic customers secured; debt of many local businesses largely written off 2009: Welfare Watch - monitor social impact of crisis, advice State institutions, coordinate targeted interventions on the ground.")

27

President Ólafur Ragnar Grímsson: “two fundamental dilemmas” “First, how far, if at all, the state should be forced to shoulder the responsibility for debt created by private banks. Or, to put it differently: Should ordinary people, the nation, be responsible for bad management of private financial institutions, especially if the potential losses are due to operations in foreign countries? Should we have a banking system which privatises the profits but socialises the losses and turns private failures into sovereign debt? The second dilemma goes to the heart of our democracies: if a conflict arises between the interests of the financial markets and the will of the people, which should reign supreme: the market or the people? “ Speech by the President of Iceland, Ólafur Ragnar Grímsson, at the 8th UNCTAD Debt Management Conference Geneva, 14th November 2011, pp.2f

28

Kurz doch sehr informativ über Islands erfolgreiche Krisenbewältigung und die Unterschiede zur menschen- verachtenden und ineffizienten Katstrophenpolitik der EU und der Troika : Juan Pablo Bohoslavsky (2014) “End-of-mission statement by Mr. Juan Pablo Bohoslavsky, United Nations Independent Expert on the effects of foreign debt and other related international financial obligations of States on the full enjoyment of all human rights, particularly economic, social and cultural rights. Mission to Iceland, 8-15 December 2014”, http://www.ohchr.org/EN/NewsEvents/Pages/DisplayNews.aspx?Ne wsID=15420&LangID=E

29

“Given Greece’s high debt levels, resolving its balance of payments problem within the euro will require debt relief and long-term transfers from its European partners.” IMF (2012) IMF Country Report No. 12/57, March 2012, p.14 Solidarity with the Greek? “Vulture funds stand to make a fortune from a second Greek bailout after buying hundreds of millions of euros of distressed sovereign debt in the past few months.” The Telegraph, Philip Aldrick, 25 June 2011 Robert Marquardt, founder of Signet, a fund of hedge funds: Greek crisis "certainly a great chance to make money". (ibid) 2 nd private haircut: hedge funds bought distressed debt at <15% German idea (escrow account) to restrict future payments to re-payment of creditors ▬► further socialising losses and “repaying” public claims from one’s own public pocket; danger to democracy and parliamentary rights

2 nd private haircut: hedge funds bought distressed debt at <15% German idea (escrow account) to restrict future payments to re-payment of creditors ▬► further socialising losses and repaying public claims from one’s own public pocket; danger to democracy and parliamentary rights.")

30

Early on: proposals to reduce Greek debts instead of delaying insolvency by illegal bailouts, e.g., Gros and Mayer (February 2010) : 50% off, EMF Mohamed El-Erian: “debt trap”, debts < 90%; burden equally shared, not just have taxpayers cough up the money Gianviti, Krueger, Pisani-Ferry, Sapir, von Hagen (2010) Raffer (2010 – first time proposed 1987 at Zagreb University) even Berlin Club briefly considered (German government) EU-specific problem : public sector pushed bona fide private creditors into lending to “problem countries”: Basel Agreements; EU (capital requirements directives); large exposure regime excludes highly rated sovereigns from the 25% of equity limit Soros (FT), banks “obliged to hold riskless assets to meet their liquidity requirements were induced to load up on the sovereign debt of the weaker countries to earn a few extra basis points”

: 50% off, EMF Mohamed El-Erian: debt trap , debts < 90%; burden equally shared, not just have taxpayers cough up the money Gianviti, Krueger, Pisani-Ferry, Sapir, von Hagen (2010) Raffer (2010 – first time proposed 1987 at Zagreb University) even Berlin Club briefly considered (German government) EU-specific problem : public sector pushed bona fide private creditors into lending to problem countries : Basel Agreements; EU (capital requirements directives); large exposure regime excludes highly rated sovereigns from the 25% of equity limit Soros (FT), banks obliged to hold riskless assets to meet their liquidity requirements were induced to load up on the sovereign debt of the weaker countries to earn a few extra basis points")

Ähnliche Präsentationen

András Bárdossy IWS Universität Stuttgart.>")

but young men are no.>")