Präsentation herunterladen

Die Präsentation wird geladen. Bitte warten

1

040589 VO Grundlagen der Entwicklungsökonomie WS 2013-14

VL-Unterlagen (PPT) zu VO Grundlagen der Entwicklungsökonomie WS Kunibert Raffer © K Raffer 2013

zu VO Grundlagen der Entwicklungsökonomie. WS Kunibert Raffer. © K Raffer")

2

© K Raffer 2013

3

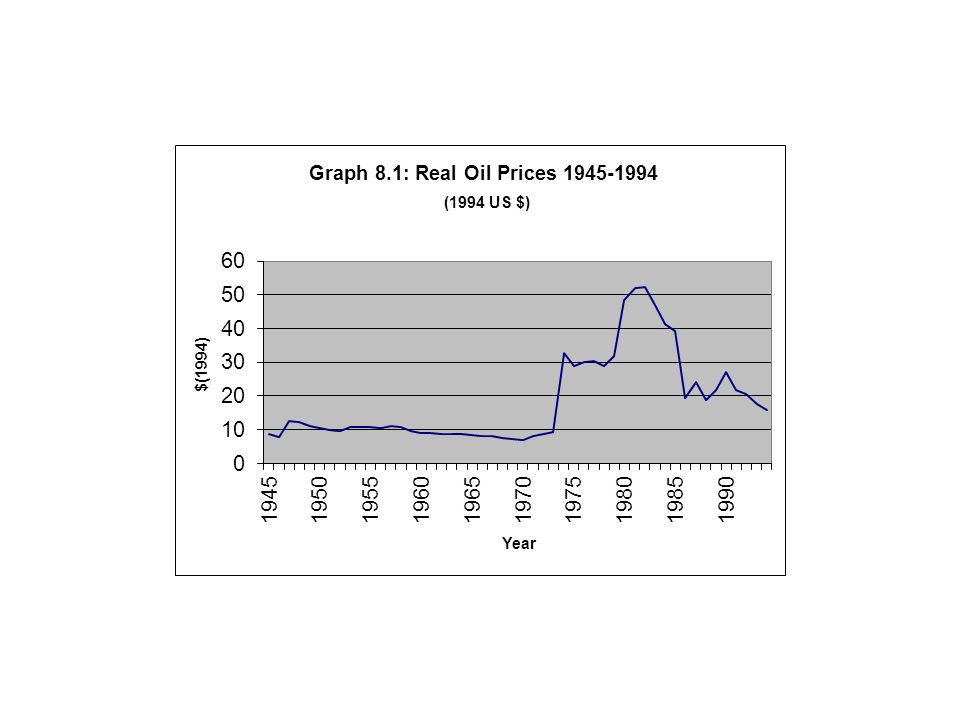

0 ≤ DSR/DSRd* ≤ 1 DSR is the IBRD’s cash-base ratio.

DSRd*, is debt service paid plus payments due but not effected. My index - which for the sake of brevity and want of any better name might be called Raffer index - is 1 if all payments are made on time, zero if nothing is paid. Multiplied by 100 it shows actual payments as percentages of debt service due © K Raffer 2013

4

Table A.3: Sub-Saharan Africa's Arrears and Debt Service 1980-1993

(%) p Debt- (DSR) and Interest-Service-Ratios (ISR) on Cash Base* WDT ISR DSR WDT ** ISR DSR Contractual DSR and ISR*** ISRd DSRd ISRd DSRd * DSR = Debt Service Ratio: (actual) total debt service/exports of goods and services (TDS/XGS); ISR = Interest Service Ratio: (actual) interest payments (INT/XGS) ** Data for 1992 provisional estimates *** d indicates that actual payments plus arrears are used in the numerator p projected Source: WDT ,

p. Debt- (DSR) and Interest-Service-Ratios (ISR) on Cash Base* WDT ISR DSR WDT ** ISR DSR Contractual DSR and ISR*** ISRd DSRd ISRd DSRd * DSR = Debt Service Ratio: (actual) total debt service/exports of goods and services (TDS/XGS); ISR = Interest Service Ratio: (actual) interest payments (INT/XGS) ** Data for 1992 provisional estimates. *** d indicates that actual payments plus arrears are used in the numerator. p projected. Source: WDT ,")

5

Somalia: Growth Rates of GDP and Livestock GDP, Selected Periods

(per cent per annum) (3 yrs) (2 yrs) (1 yr) (1 yr) (1 yr) (1 yr) GDP at factor costs IMF IBRD n.a n.a. National I Nation. II Livestock GDP National I Nation. II Source: Jamal 1992, p.144

(3 yrs) (2 yrs) (1 yr) (1 yr) (1 yr) (1 yr) GDP at factor costs. IMF IBRD n.a. n.a. National I Nation. II Livestock GDP. National I Nation. II Source: Jamal 1992, p.144.")

6

and Development Thinking

HARROD-DOMAR and Development Thinking s/k = g = n s rate of savings k capital output ratio g rate of growth n population growth

7

Washington Consensus (John Williamson) Fiscal discipline: (typically a primary budget surplus of several percent of GDP) Public expenditure priorities (high economic returns; primary health, education) Tax reform (especially cutting marginal tax rates) Financial liberalization (moderately positive real interest rates, no preferential interest rates) Exchange rates (unified and competitive) Trade liberalization (?slowing down during crises) Foreign direct investment (equal treatment) Deregulation Privatization Property rights

Tax reform (especially cutting marginal tax rates) Financial liberalization (moderately positive real interest rates, no preferential interest rates) Exchange rates (unified and competitive) Trade liberalization ( slowing down during crises) Foreign direct investment (equal treatment) Deregulation. Privatization Property rights.")

8

The obstinate conservatism with which the classical comparative cost thinking has been retained in theory as something more than a pedagogical introduction - or a model for the treatment of a few special problems - is evidence that, even today, there is in many quarters an insufficient understanding of this fundamental fact. It follows that not only the comparative cost model but also the factor proportions model can only be applied in special cases and used as a general introduction to illuminate the character of trade in some essential aspects ... It is characteristic of the developing countries that a good many factors do not exist at all and that the quality of others differs from factors in the industrialized countries. This means that a simple method of analysis - such as the factor proportions model - which does not take this into account is to some extent unrealistic. Bertil Ohlin (1967) Interregional and International Trade, Cambridge (Mass), Harvard UP 308f. (stress in or.)

Interregional and International Trade, Cambridge (Mass), Harvard UP 308f. (stress in or.)")

9

Production Changes (LUs used to produce C and W respectively)

Table 1.a: Graham's Case (Viner's presentation) Basic Assumptions: Countries A and B both have 400 Units of (nationally standardised, or homogeneous) Labour (LU); the international price ( net barter terms of trade) remains at 4C = 3.5W (Pintl = 0.875) 1) Constant Returns (Ricardian-Torrens) Case: A B production per LU ( productivity) C 4 4 W 4 3 Pb = 0.75 (4C = 3W) Pintl = Pa = 1 Production Changes (LUs used to produce C and W respectively) Specialisation I Specialisation II Total Specialisation Country A B (A+B) A B Differ*) A B Diff.*) C (LU) (200) (200) (100) (300) (400) W (LU) (200) (200) (300) (100) (400)

Basic Assumptions: Countries A and B both have 400 Units of (nationally standardised, or homogeneous) Labour (LU); the international price ( net barter terms of trade) remains at 4C = 3.5W (Pintl = 0.875) 1) Constant Returns (Ricardian-Torrens) Case: A B. production per LU ( productivity) C 4 4. W 4 3. Pb = 0.75 (4C = 3W) Pintl = Pa = 1. Production Changes (LUs used to produce C and W respectively) Specialisation I Specialisation II Total Specialisation. Country A B (A+B) A B Differ*) A B Diff.*) C (LU) (200) (200) (100) (300) (400) W (LU) (200) (200) (300) (100) (400)")

10

Table 1.b: Graham's Case (Viner's presentation)

Specialisation (II) Specialisation (III) A B A B C 4.5 3, W 0.571 < Pintl = < < Pintl = < 1 Production changes: Specialisation II Specialisation III Total Specialisation. A B Diff.*) A B Diff.*) A B Diff.*) C , , (LU) (100) (300) (1) (399) (400) W , , (LU) (300) (100) (399) (1) (400) *) compared with Specialisation I

Specialisation (III) A B A B. C 4.5 3, W < Pintl = < < Pintl = < 1. Production changes: Specialisation II Specialisation III Total Specialisation. A B Diff.*) A B Diff.*) A B Diff.*) C , , (LU) (100) (300) (1) (399) (400) W , , (LU) (300) (100) (399) (1) (400) *) compared with Specialisation I.")

11

Unequal Exchange : DFToT ≠ 1

Austauschverhältnisse (Terms of Trade) 1) Commodity or Net-Barter ToT: Px/Pm Px price (index) of exports Pm price (index) of imports 2) Double Factoral (US: Factorial) ToT PxNx/PmNm NBToT weighted by productivity indices (N); compare rewards of homogeneous factor units Unequal Exchange : DFToT ≠ 1 Income ToT: PxQx/Pm Qx exported quantity; real export income Gross Barter ToT: Qx/Qm Single Factoral ToT (only exports weighted with Nx ) Employment Corrected DFToT: PxNx multiplied by index of employment in developing country (cf. Spraos 1983; Singer 1989)

1) Commodity or Net-Barter ToT: Px/Pm. Px price (index) of exports Pm price (index) of imports. 2) Double Factoral (US: Factorial) ToT. PxNx/PmNm. NBToT weighted by productivity indices (N); compare rewards of homogeneous factor units. Unequal Exchange : DFToT ≠ 1. Income ToT: PxQx/Pm. Qx exported quantity; real export income. Gross Barter ToT: Qx/Qm. Single Factoral ToT (only exports weighted with Nx ) Employment Corrected DFToT: PxNx multiplied by index of employment in developing country (cf. Spraos 1983; Singer 1989)")

12

|i| = - |wi| - erij srj si-1

Ungleicher Tausch: Produktspezifizität und Preisdurchsetzungsmacht |i| = - |wi| - erij srj si-1 i Spezifische Elastizität eines Exportgutes des Landes i wi Kreuzpreiselastizität der Weltnachfrage erij Kreuzpreiselastizitäten des Angebots aller anderen Quellen srj Anteil am Gesamtangebot si Anteil des Exportlandes i am Weltexport

13

Unterschiede zu den üblichen Elastizitätsschätzungen

Bogenelastizitäten Substitution hängt von Verfügbarkeit (auch im Sinne wirtschaftlicher Vertretbarkeit) ab Zeitabhängig (Reaktionszeit)

ab. Zeitabhängig (Reaktionszeit)")

14

Definition Official Development Assistance (ODA):

"those flows to developing countries and multilateral institutions provided by official agencies, including state and local governments, or by their executive agencies, each transaction of which meets the following tests: a) it is administered with the promotion of the economic development and welfare of developing countries as its main objective, and b) it is concessional in character and contains a grant element of at least 25 per cent." DAC (Development Assistance Committee) der OECD Zuschußelement (grant element): Unterschied OEH-Kredit und Kredit mit 10% Zinsen (gemessen in Kapitalwerten) Beispiele, gerade >25% (OECD 1985, p.172): - 4 %, 7 Jahre Laufzeit, 3 Jahre tilgungsfrei - 5 %, 11 Jahre Laufzeit, 4 Jahre tilgungsfrei - 5 %, 15 Jahre Laufzeit, keine tilgungsfreie Zeit

it is administered with the promotion of the economic development and welfare of developing countries as its main objective, and. b) it is concessional in character and contains a grant element of at least 25 per cent. DAC (Development Assistance Committee) der OECD. Zuschußelement (grant element): Unterschied OEH-Kredit und Kredit mit 10% Zinsen (gemessen in Kapitalwerten) Beispiele, gerade >25% (OECD 1985, p.172): - 4 %, 7 Jahre Laufzeit, 3 Jahre tilgungsfrei. - 5 %, 11 Jahre Laufzeit, 4 Jahre tilgungsfrei. - 5 %, 15 Jahre Laufzeit, keine tilgungsfreie Zeit.")

15

DAC -ODA (%) 2012: provisional Source: DAC

2012: provisional Source: DAC")

16

Broadened and Deflated Totals

ODA by DAC Members Broadened and Deflated Totals (% of GSP) DAC-value *) minus admin. costs refugees emerg.& dis.relief emergency food aid debt forgiveness capital subscr contrib. to NGOs students (imputed) former Commun. C ODA-Inflator Sources: Raffer (1998), based on OECD-data (various publications)

DAC-value *) minus. admin. costs refugees emerg.& dis.relief emergency food aid debt forgiveness capital subscr contrib. to NGOs students (imputed) former Commun. C ODA-Inflator Sources: Raffer (1998), based on OECD-data. (various publications)")

17

Broadened and Deflated Totals

ODA by DAC Members Broadened and Deflated Totals (% of GSP) Official DAC-value Deflated ODA ODA-Inflator Source: Raffer 1998a Table 6.2: Corrected ODA and OA by DAC Members (% of GSP) Deflated ODA OA Total Quelle: Raffer & Singer 2001/2004, p.89

Official DAC-value Deflated ODA ODA-Inflator Source: Raffer 1998a. Table 6.2: Corrected ODA and OA by DAC Members. (% of GSP) Deflated ODA OA Total Quelle: Raffer & Singer 2001/2004, p.89.")

19

Country Programmable Aid (CPA)

“is the portion of aid donors programme for individual countries, and over which partner countries could have a significant say. Developed in 2007 in close collaboration with OECD DAC members, CPA is much closer to capturing the flows of aid that go to the partner countries than the concept of Official Development Assistance (ODA).” Source: OECD CPA: “(1) inherently unpredictable (such as humanitarian aid and debt relief); or (2) entails no flows to the recipient country (administration, student costs, development awareness and research and refugee spending in donor countries); or (3) is usually not discussed between the main donor agency and recipient governments (food aid, aid from local governments, core funding to international NGOs, aid through secondary agencies, ODA equity investments and aid which is not allocable by country). Finally, (4), CPA does not net out loan repayments, as these are not usually factored into aid allocation decisions.”

. Source: OECD. CPA: (1) inherently unpredictable (such as humanitarian aid and debt relief); or. (2) entails no flows to the recipient country (administration, student costs, development awareness and research and refugee spending in donor. countries); or. (3) is usually not discussed between the main donor agency and recipient. governments (food aid, aid from local governments, core funding to. international NGOs, aid through secondary agencies, ODA equity investments. and aid which is not allocable by country). Finally, (4), CPA does not net out loan repayments, as these are not usually factored. into aid allocation decisions.")

20

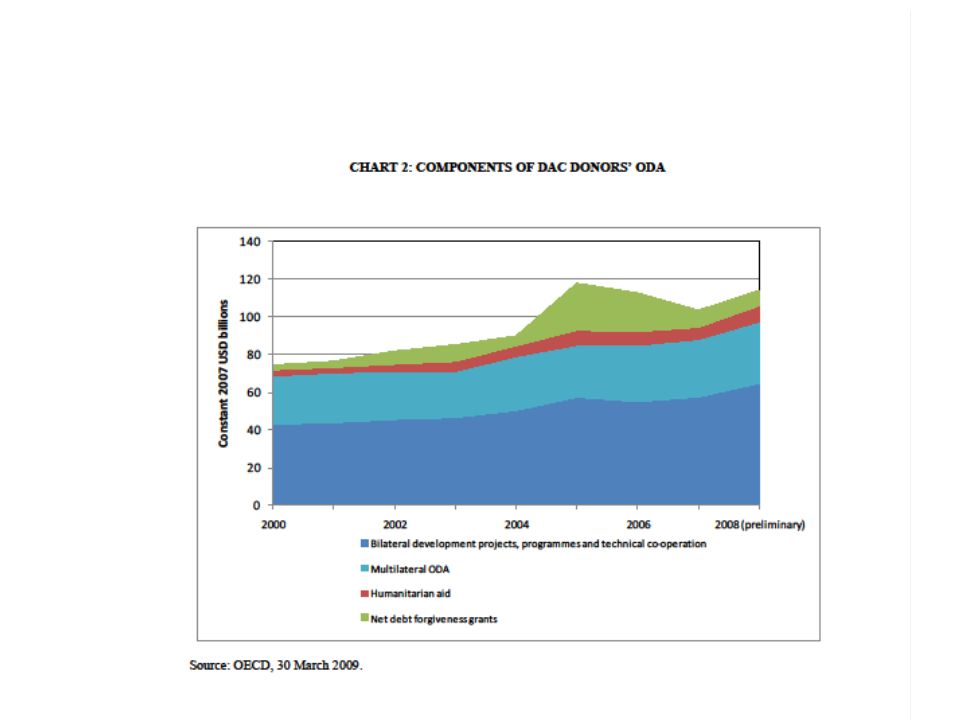

ODA Composition 2011 Source: OECD 2013

21

The Millennium Development Goals

Eight Goals for 2015 1. Eradicate extreme poverty and hunger 2. Achieve universal primary education 3. Promote gender equality and empower women 4. Reduce child mortality 5. Improve maternal health 6. Combat HIV/AIDS, malaria and other diseases 7. Ensure environmental sustainability 8. Develop a global partnership for development Goal 1. Eradicate extreme poverty and hunger Target 1: Reduce by half the proportion of people living on less than a dollar a day Indicators: 1. Proportion of population below $1 (PPP) per day 2. Poverty gap ratio, $1 per day 3. Share of poorest quintile in national income or consumption Target 2: Reduce by half the proportion of people who suffer from hunger 4. Prevalence of underweight children under five years of age 5. Proportion of the population below minimum level of dietary energy consumption

per day. 2. Poverty gap ratio, $1 per day. 3. Share of poorest quintile in national income or consumption. Target 2: Reduce by half the proportion of people who suffer from hunger. 4. Prevalence of underweight children under five years of age. 5. Proportion of the population below minimum level of dietary energy consumption.")

22

Paris Declaration on Aid Effectiveness (2005)

1. Ownership: Developing countries set their own strategies for poverty reduction, improve their institutions and tackle corruption. 2. Alignment: Donor countries align behind these objectives and use local systems. 3. Harmonisation: Donor countries coordinate, simplify procedures and share information to avoid duplication. 4. Results: Developing countries and donors shift focus to development results and results get measured. 5. Mutual accountability: Donors and partners are accountable for development results. Accra Agenda for Action (2008) Ownership Inclusive partnerships: All partners - including donors in the OECD DAC and developing countries, as well as other donors, foundations and civil society - participate fully. Delivering results: Aid is focused on real and measurable impact on development. Capacity development: ability of SCs to manage own future - also lies at the heart of AAA

Ownership. Inclusive partnerships: All partners - including donors in the OECD DAC and developing countries, as well as other donors, foundations and civil society - participate fully. Delivering results: Aid is focused on real and measurable impact on development. Capacity development: ability of SCs to manage own future - also lies at the heart of AAA.")

23

Busan Partnership (2011) “result of an inclusive year-long process of consultation” – “sets out principles, commitments and actions that offer a foundation for effective co-operation in support of international development.” Is the Busan Partnership document legally binding? How will implementation be ensured? “The Busan Partnership document does not take the form of a binding agreement or international treaty. It is not signed, and does not give rise to legal obligations. Rather, it is a statement of consensus that a wide range of governments and organisations have expressed their support for, offering a framework for continued dialogue and efforts to enhance the effectiveness of development co-operation. The Busan Partnership document foresees the establishment of a Global Partnership for Effective Development Co-operation, which will support and help ensure accountability for implementation at the political level. A light framework will be agreed through which progress will be monitored and mutual accountability supported.”

25

IFI SIND NICHT BEVORZUGTE GLÄUBIGER

IWF nachzulesen auf IWF-homepage (auf Seite 820 des Files): Rutsel-Sylvestre (1990): Gründer(innen) des IMF stipulierten NACHRANGIGKEIT der Fondsforderungen; explizite Nachrangigkeit (Schedule B, paragraph 3) mit 2. Statutenänderung verschwunden SDRM war der Versuch, sich die wider besseres Wissen behauptete rechtliche Bevorzugung endlich und insbesondere zu Lasten des privaten Sektors zu erschleichen Folgen des Verhinderns von Haftung, Rechtsstaatlichkeit und marktwirtschaftlicher Prinzipien: “IFI flops securing IFI jobs” (Raffer 1993) steigende Verschuldung der EL, erschwertes “Schuldenmanagement”, aber mehr Einkommen und Einfluß für IWF ökonomisch perverses Anreizsystem

: Rutsel-Sylvestre (1990): Gründer(innen) des IMF stipulierten NACHRANGIGKEIT der Fondsforderungen; explizite Nachrangigkeit (Schedule B, paragraph 3) mit 2. Statutenänderung verschwunden. SDRM war der Versuch, sich die wider besseres Wissen behauptete rechtliche Bevorzugung endlich und insbesondere zu Lasten des privaten Sektors zu erschleichen. Folgen des Verhinderns von Haftung, Rechtsstaatlichkeit und marktwirtschaftlicher Prinzipien: IFI flops securing IFI jobs (Raffer 1993) steigende Verschuldung der EL, erschwertes Schuldenmanagement , aber mehr Einkommen und Einfluß für IWF ökonomisch perverses Anreizsystem.")

26

b) Blumenthal Bericht (Zaire 1982)

Beispiele: a) J. Stiglitz: IWF soll umfangreiche Textpassagen aus Dokument für Land A in Dokument über Land B eingefügt haben (manchmal vergessen Namen zu ändern) b) Blumenthal Bericht (Zaire 1982) c) Asienkrise: IBRD (1999) GAB offiziell ZU Jahre vorher gewußt zu haben, daß von IFI stark propagierte, rasche Liberalisierung wieder Krise auslösen würde; warnte Mitglieder aber nicht! IWF MUSZTE es WISSEN (Chile Crash!) IMF-IEO (2004) The IMF and Argentina, 1991–2001 “program was also based on policies that were either known to be counterproductive ... or that had proved to be ‘ineffective and unsustainable everywhere they had been tried’ ... [A]s expressed by FAD [Fiscal Affairs Department] at the time.” (p.91) Board unterstützte “a program that Directors viewed as deeply flawed” (pp.81f) - “September 2001 augmentation suffered from a number of weaknesses in pro-gram design, which were evident at the time. If the debt were indeed unsustain-able, as by then well recognized by IMF staff, the program offered no solution to that problem.” (p.89, Herv. KR) – IWF "staff estimates“, Schuldenreduktion zwischen 15 und 40% wäre nötig ▬►crédito abusivo (J.P. Bohoslavsky)

J. Stiglitz: IWF soll umfangreiche Textpassagen aus Dokument für Land A in Dokument über Land B eingefügt haben (manchmal vergessen Namen zu ändern) b) Blumenthal Bericht (Zaire 1982) c) Asienkrise: IBRD (1999) GAB offiziell ZU Jahre vorher gewußt zu haben, daß von IFI stark propagierte, rasche Liberalisierung wieder Krise auslösen würde; warnte Mitglieder aber nicht! IWF MUSZTE es WISSEN (Chile Crash!) IMF-IEO (2004) The IMF and Argentina, 1991– program was also based on policies that were either known to be counterproductive ... or that had proved to be ‘ineffective and unsustainable everywhere they had been tried’ ... [A]s expressed by FAD [Fiscal Affairs Department] at the time. (p.91) Board unterstützte a program that Directors viewed as deeply flawed (pp.81f) - September 2001 augmentation suffered from a number of weaknesses in pro-gram design, which were evident at the time. If the debt were indeed unsustain-able, as by then well recognized by IMF staff, the program offered no solution to that problem. (p.89, Herv. KR) – IWF staff estimates , Schuldenreduktion zwischen 15 und 40% wäre nötig ▬►crédito abusivo (J.P. Bohoslavsky)")

27

Haftung, Schadenersatz

IWF laut Art. IX, Abs 3: vollständige Immunität “except to the extent that it expressly waives its immunity for the purpose of any proceedings or by the terms of any contract” Schiedsgerichtliches Verfahren (wie zB IBRD) zur Feststellung ob Haftungsgründe vorliegen, ob bzw. wie viel Schadenersatz an rechtswidrig geschädigte Mitglieder zu zahlen ist. Risikovorsorge („precautionary reserves“) Alle IFI außer IWF statutarisch verpflichtet, auch IWF hat vorgesorgt - ALLE haben Kunden Kosten der Risikoabsicherung verrechnet, weigern sich aber die schon bezahlte Versicherungsleistung zu gewähren

zur Feststellung ob Haftungsgründe vorliegen, ob bzw. wie viel Schadenersatz an rechtswidrig geschädigte Mitglieder zu zahlen ist. Risikovorsorge („precautionary reserves ) Alle IFI außer IWF statutarisch verpflichtet, auch IWF hat vorgesorgt - ALLE haben Kunden Kosten der Risikoabsicherung verrechnet, weigern sich aber die schon bezahlte Versicherungsleistung zu gewähren.")

Ähnliche Präsentationen